Subscribe to newsletter

Subscribe to newsletter

05/06/2020

On June 5th the Australian Financial Review published an article highlighting what some CEOs have taken home over time.

The ranking was based on well-established research methods used by proxy adviser Ownership Matters (SEE HERE).

A similar method is employed by ISS and Glass Lewis in overseas jurisdictions, where they directly contrast multiple years’ take home pay with TSR performance.

We expect that eventually all Australian proxy advisers and their clients will be applying this as a test of remuneration committee and board competence.

Currently, ISS in Australia predominantly considers statutory values. CGI Glass Lewis and Ownership Matters draw on multiple methodologies, but both take into account a version of realisable pay. (Note: Ownership Matters’ methodology is a mix of realised pay and realisable pay, since it considers the intrinsic value of options on exercise, but share rights at vesting.)

Realisable pay (the intrinsic value, or potential cash in the pocket, on the day pay vests) or realised pay (the value of cash salary plus options and rights when actually exercised for cash) have become increasingly important to investors when deciding their say on pay vote. It is considered as the “actual” value of remuneration for the year and is often compared to company performance.

Consider the ACSI CEO pay report for ASX 200 companies that is published each year (See HERE) and identifies the top 10 executives by realised pay (based on Ownership Matters research.)

Companies have responded by putting more prominence on this methodology in their remuneration reports by introducing a realisable remuneration table (See HERE).

The table is non-statutory and therefore companies present different versions of realisable pay depending on their preferences and remuneration framework. For example, some might include the STI cash paid in the year rather than the STI cash to be awarded based on performance in that year and vice versa. Guerdon Associates has conducted analysis in the variation in voluntarily disclosed realisable tables and understands the rationale, merits and flaws behind the different approaches.

While target and maximum remuneration opportunities are commonly benchmarked across companies, realisable pay is benchmarked much less frequently. It requires greater expertise and larger investment of time (and therefore expense). The calculation involves multiple complexities, including the treatment of dividends.

Guerdon Associates frequently undertakes this benchmarking for clients genuinely interested in how well policy has been implemented for alignment with shareholders over time. Coincidently, it prepares the chair of the remuneration committee to engage constructively with proxy advisers and investors. Often, the results are illuminating for identifying which of their peers manage executive pay well, and how they compare.

There are advantages to knowing peers’ realisable pay and TSR performance over time such as:

- learning the actual remuneration value attained by competitors;

- providing assistance for engagement with investors who traditionally look to other methodologies (statutory, target or maximum), showing another perspective on how much remuneration the company’s executive earns (See HERE) AND HERE); This is especially useful in assessing the case for board discretion on pay matters.

- taking the difficulty of performance conditions into account in benchmarking. A company may be at a disadvantage regarding recruitment and retention by having more difficult performance conditions than peers;

- providing a tool to compare remuneration against performance by looking at total realisable pay and TSR over multiple years, as is practice by ISS and Glass Lewis in several countries.

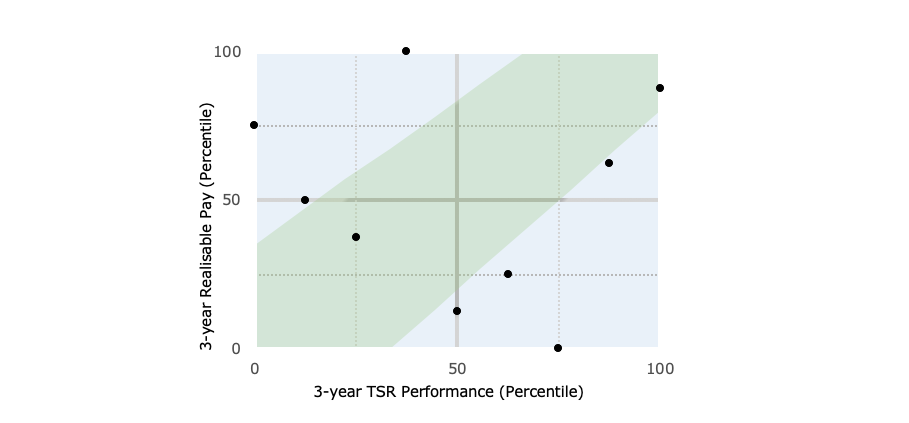

Guerdon Associates expects that in the future this approach will be used by all Australian proxy advisors. The graph below is an example for Australian companies in one industry.

The green area represents the area where realisable pay and performance are aligned for the peers. Below the green area are the peers that have high TSR but lower relative realisable pay. These companies are at a competitive disadvantage to their peers – a high performing executive may consider leaving for another company where their performance is better remunerated. Above the green area are the peers that have low TSR but higher relative realisable pay, which will raise red flags for proxy advisers.

Figure 1: Performance vs Realisable Pay Graph for example Australian Industry

As can be seen, there are few companies in this sample who are meeting the green corridor “sweet spot”. Would yours be one?

By benchmarking realisable pay weaknesses can be identified, alterations can be made to ensure pay falls within the green area.

© Guerdon Associates 2024 Back to all articles

Back to all articles