Subscribe to newsletter

Subscribe to newsletter

ESG measures in mining companies unearthed and compared globally

07/09/2020

The GECN Group research study explored Environmental, Social and Governance (ESG) measures in global executive remuneration (see the summary outcome HERE). In this article, we dig into the ESG measures used by the leading Metals & Mining companies in Australia (ASX 100 including BHP and Rio Tinto), Canada (S&P/TSX 60) and the United Kingdom (FTSE 100 excluding BHP and Rio Tinto).

Types of ESG metrics

Incorporating ESG measures in executive incentive plans signals the company’s intention to reflect ESG performance in remuneration outcomes.

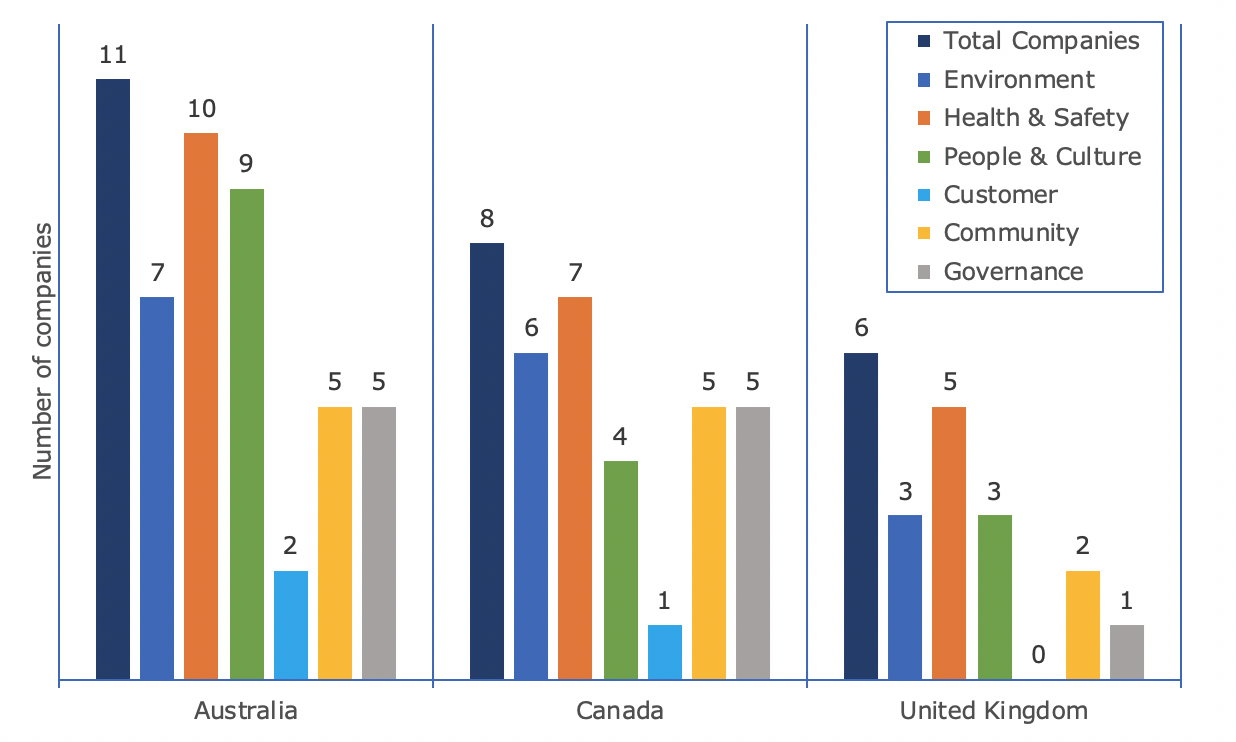

Figure 1 shows the various types of ESG metrics used in executive incentive plans.

Figure 1: Number of mining companies with various ESG metrics

Pay impact of ESG metrics$

While simply incorporating ESG metrics in incentive plans may meet external stakeholder and investor requirements, their effectiveness in incentivising management performance will largely depend on their weighting within the overall remuneration package.

That is, ESG metrics with a low weighting and impact on remuneration outcomes will probably tend to be ignored by executives who will assess the relative effort and reward for achieving targets for each incentive metric.

Figure 2 shows the average remuneration mix of mining CEOs with ESG measures.

Figure 2: Average remuneration mix of mining CEOs with ESG metrics

The aggregate weighting of ESG metrics within Australian mining companies determines up to 15% of the CEO’s overall remuneration outcomes. While the average impact of ESG metrics on remuneration outcomes is higher for Australia relative to overseas peers, there is still a larger emphasis on financial and non-ESG metrics in determining the majority of incentive outcomes.

ESG metrics in STI outcomes assessment

The two main approaches for incorporating ESG metrics in STI outcomes are:

1. ESG metrics within a balanced scorecard and a pre-determined weighting;

2. ESG metrics as a modifier adjusting the outcome of a balanced scorecard.

A balanced scorecard approach awards a portion of the STI opportunity based on ESG performance irrespective of financial performance. If ESG performance is poor, an STI payout could still be received for non-ESG performance.

An ESG modifier approach adjusts a scorecard outcome based on ESG performance. If ESG performance is poor, it affects outcomes on all STI measures, including financial. A modifier approach makes it clear to management that financial performance should not come at the cost of ESG performance, and vice versa.

Figure 3 shows how mining companies are incorporating ESG metrics in determining STI outcomes.

Figure 3: ESG metrics in assessing mining company STI outcomes

Most mining companies in Australia and Canada incorporate ESG metrics in the STI scorecard only. Half of the mining companies in the United Kingdom incorporate ESG metrics in determining their balanced scorecard outcome as well as a modifier adjusting the scorecard outcome.

Conclusions

Australian-listed mining CEO remuneration places higher weight on ESG factors than foreign-listed mining company CEO remuneration. However, UK CEOs’ ESG performance may impact remuneration outcomes based on financial and other non-ESG factors more than equivalents in Canada or Australia.

Methodology

ESG measures in executive incentive plans were grouped into six categories based on the metrics disclosed:

- Environmental measures include emissions, energy management, environmental incidents, and water and waste management.

- Health and safety measures include fatalities, injuries, illnesses and other workplace safety policies

- People and culture measures include diversity and inclusion, employee engagement, training and development, and behaviour and culture.

- Customer measures include customer satisfaction, customer complaints and resolutions and product quality and safety.

- Community measures include community incidents, community complaints, and social investments.

- Governance measures include succession planning, external stakeholder management, risk management, compliance, and company ethics and values.

The maximum annual policy remuneration mix was determined for mining CEOs based on four remuneration components:

1. ESG Incentives is the aggregated weighting of individual ESG metrics in incentive plans

2. Non-ESG Incentives is the aggregated weighting of incentive metrics without any ESG components and includes both financial metrics and non-financial metrics that are not ESG related

3. Non-Performance Equity includes any time-vested or service-vested equity granted without any performance conditions

4. Cash Salary includes any fixed cash remuneration

© Guerdon Associates 2026 Back to all articles

Back to all articles