Subscribe to newsletter

Subscribe to newsletter

Do LTI measures drive ASX 100 share buybacks?

13/05/2019

Earnings per share (EPS) is a common and accepted performance measure for long-term incentive plans: it is well defined and understood, it is transparent if based on statutory net profit, and analyst forecasts are often readily available to benchmark vesting requirements.

A potential concern for investors is that EPS and other common LTI measures such as cash flow per share (CFPS) and return on equity (ROE) can be improved without necessarily improving the earnings power of the business, as incentive plan targets can be met in the short and medium term by repurchasing shares instead of investing in the long-term prospects of the business. Share buybacks in the US have frequently been criticised for this reason, where companies are accused of attempting to inflate EPS instead of investing in capital projects and R&D.

To test whether executives in Australian companies have repurchased shares in an attempt to inflate LTI measures and meet performance targets, we recently analysed the cash spending of ASX 100 companies from FY 2016 to FY 2018.

After excluding four companies which de-listed during the period, 52 of the remaining 96 companies in the sample had performance measures based on EPS, CFPS or ROE in their FY 2016 LTIs which could benefit from share buybacks (referred to as “Buyback measures” below).

The average performance period of these LTIs was 3 years with vesting in FY 2018. If executives were forgoing investment opportunities to instead repurchase shares to meet their performance targets, we would expect companies with these LTI measures to have spent a higher proportion of total cash outlays on buybacks over FY 2016 to FY 2018 relative to companies without such measures in their FY 2016 LTIs.

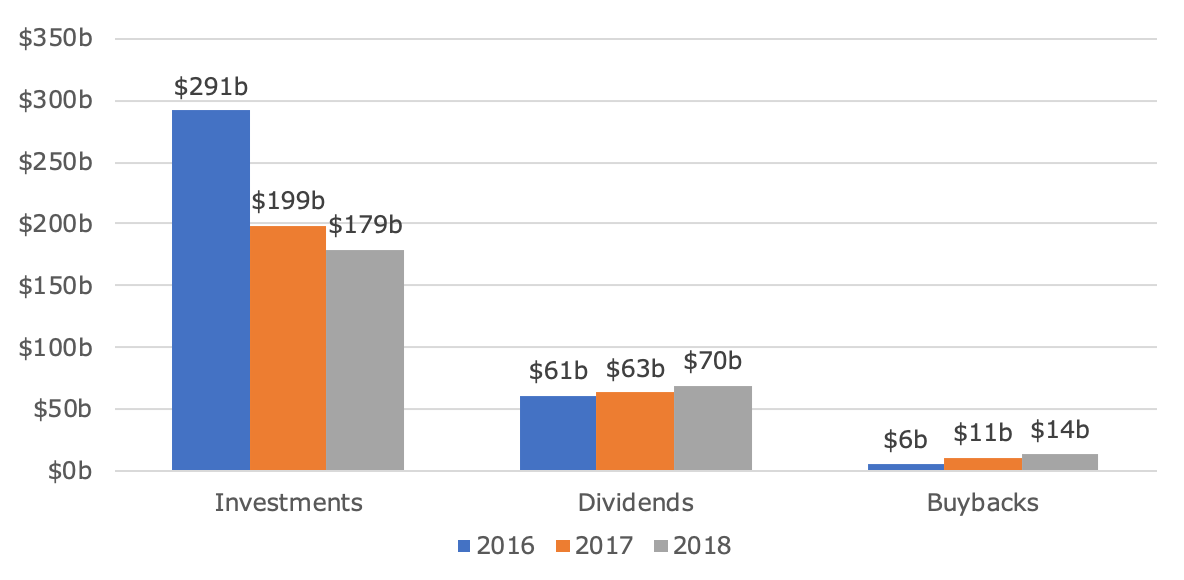

The sample companies spent an aggregate $670 billion on investments (capex, R&D and cash acquisitions) during the analysed period, whilst returning $194 billion to shareholders in the form of dividends and $31 billion in net share buybacks.

Figure 1: ASX 100 total cash spending FY 2016 to FY 2018

Whilst the aggregate amount spent on investments declined from $291 billion in FY 2016 to $179 billion in FY 2018, annual distributions to shareholders in the form of dividends and buybacks increased during the period.

The number of companies doing a buyback increased from 36 in FY 2016 to 47 in FY 2018, with the aggregate amount increasing from $6 billion to $14 billion.

Was this increase in buybacks on the ASX 100 driven by LTI measures? Probably not: the 52 companies with buyback measures only accounted for $7.3 billion (24%) of total buybacks in the period, and the average company with buyback measures also spent a smaller proportion of total cash outlays on share buybacks (1.7%) than the average company without such targets (5.2%).

After adjusting for difference in market capitalisation, the proportion of total cash outlays spent on buybacks for the average company with buyback measures went down even further.

Table 1: ASX 100 cash outlay during 2016-2018 by LTI measure

Table 2: Total cash outlay during 2016-2018

For each company, the total cash outlay during FY 2016 to FY 2018 was proportioned by the amount spent on investments, dividends and share buybacks. As shown by Tables 3 and 4, the average company with buyback measures spent relatively more on investments and less on share buybacks during the period compared with companies without such measures.

Table 3: Average proportion of total cash outlay spending purpose

Table 4: Market capitalisation weighted average proportion of total cash outlay

We think it’s safe to say that ASX 100 executives have not tried to “game” their LTI targets by returning capital to shareholders in the form of buybacks over dividends, or by forgoing long-term investment opportunities.

From the view of shareholders, directors and executives should always seek to allocate capital to its highest-value use in order to maximise the long-term value of a company. If there are no opportunities to invest capital where it can earn a sufficiently high expected return, shareholders would prefer that companies return excess cash so that they can invest it elsewhere (or spend it).

Share buybacks can be an attractive alternative for listed companies to return capital to investors instead of paying a dividend, as long-term shareholders can choose to increase their claim on the company’s assets relative to shareholders who sell their shares back to the company. It appears that ASX 100 boards are becoming increasingly aware of this, and that shareholders have little to worry about from a governance perspective.

© Guerdon Associates 2026 Back to all articles

Back to all articles