Subscribe to newsletter

Subscribe to newsletter

LTI grants: Face Value or Fair Value?

03/03/2016

The past three years have seen a shift from granting equity based on an estimate of fair value, to granting equity based on the face value of the shares at grant date.

This practice has arisen, in large part, because proxy firms among others have increasingly used face value in their benchmarking of LTIs with a view to standardising LTI values across a range of companies, driven by concerns that “fair value” undervalues a grant.

This article examines why this practice does not provide a true benchmark and can lead to anomalous outcomes for executives and shareholders.

Face value is defined as the number of rights granted multiplied by the share price at the time of grant (the share price may be a VWAP or same day value). On the other hand, fair value incorporates discounts for dividends forgone and, in some instances, the probability of vesting. This article focuses on the discount for dividends forgone, since only a few companies now determine the number to be granted on a fair value that incorporates the likelihood of vesting.

Why does it matter?

Proxy advisers use face value as the benchmark equity value. It is both simple and transparent, and has become the most common practice for listed companies when disclosing how grant size is determined. If an executive has an LTI entitlement equal to 50% of fixed pay and fixed pay is $1m, then the LTI entitlement is $500,000. If the share price is $1, then 500,000 share rights are granted.

The problem is that face value is not necessarily an accurate measure of the value of the grant. This problem is exacerbated when the LTI in other companies is calculated on the same basis and used as a benchmark. This is because the face value of a share includes the expectation of a dividend, whereas most LTI grants have no dividend entitlement.

This distinction is of little or no consequence if the company is a low or no-yield company. However, since 80% of ASX 100 companies have a yield between 3% and 8%, it becomes really important for most companies, and their executives. And it should be important for investors wanting to know what the true cost of a grant is, and whether it is enough to attract and retain suitably qualified executives.

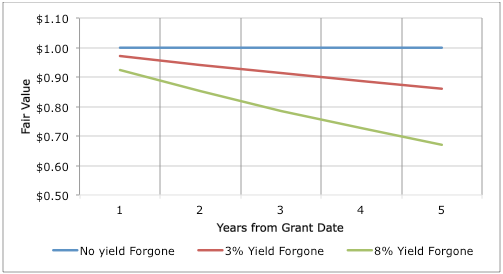

The following graph shows the present value of a $1 share with yield included and contrasts it with forgone yields of 3% and 8% over vesting periods of up to five years.

Figure 1: Impact of forgone dividends on share value

It is clear that, for high-yield companies with long vesting periods, the impact is significant. This reality is reflected in the Australian Accounting Standards Board (AASB) requirement for equity fair value, in which dividends forgone are a required input into the valuation process. The AASB 2 Application Guidance B34 states:

“When the fair value of a share grant is estimated, the valuation should be reduced by the present value of dividends expected to be paid during the vesting period.”

For example, assume that the CEO of Company A and the CEO of Company B are both granted LTI share rights with a face value of $500,000. Further:

- The Company A CEO is not entitled to dividends or their equivalent, but

- Company B CEO is entitled to dividends (awarded as additional share rights only in respect of the share rights that vest) over a four year performance period with 8% yield.

The present value of the LTI grant to the Company A CEO is $363,075 while the Company B CEO grant value is 38% higher at $500,000. However, since investors and proxy advisers, among others, focus on face value for their benchmark, their perception is that the two grants are equivalent.

Remember, our analysis ignores the probability of vesting and is only considering the difference in value of the LTI between two companies with different yields.

The impact of forgone dividends on the value of the grant extends to the stated company policy. That is, if the board’s policy is to grant equity to the value of 50% of fixed pay (say 50% of $1m, or $500,000), but then to make a grant with a value of $363,075, actually implies a policy of 36% of fixed pay.

What are the implications?

It is likely that, in addition to investors and proxy advisers, some executives and boards are unaware of the potential impact of face value grants and of the distinction with fair value. There are clear implications for equity plan design and in benchmarking methodologies.

Benchmarking can be conducted on an individual basis comparing grant values, or on a company policy basis. Simply benchmarking by comparing stated company policy could be very inaccurate, as seen in the example above where a policy of 50% can actually represent 36% of fixed pay. The benchmarking in the example above would equally be inaccurate even if both CEOs were not entitled to dividends and the companies had different yield profiles.

The benchmarking process is compromised if the comparison is not made on a like-with-like basis. This inevitably requires adjustments to equity values and stated policy values. Guerdon Associates incorporates these adjustments into the benchmarking process to ensure boards are comfortable that their company’s practice is compared accurately against the market.

The use of face value is appealing in its simplicity and has become the most common method used to determine the number of LTI rights granted. It requires little or no explanation, which is preferable to a lengthy description of a complicated process in the remuneration disclosures. The simplest way to address the disparity between face value and fair value is to remove the disparity. This involves incorporating the right to receive dividends (or an equivalent value) and may require changes to equity plan wording.

Incorporating a right to dividends does not mean that dividends are paid on unvested shares or share rights, which would be unacceptable to most investors and proxy advisers. Dividends are only accumulated to the extent that the equity grant vests.

Apart from aligning face value and fair value there is another strong rationale for incorporating dividends. If dividends are incorporated, the grant is capital neutral. That is, there is no incentive to push down dividend yield in favour of share price appreciation. For low yield companies the risk is low, but for high yield companies the potential exists for a conflict of interest. So, importantly, incorporating dividend entitlements ensures a better alignment with shareholder interests. Most share rights plans fail in this respect.

For companies that have historically determined grant value and size based on face value, the incorporation of dividends effectively increases the value of the grant. It is important to acknowledge this in disclosures so that it is not misinterpreted as a backdoor pay increase. For a CEO with fixed pay of $1m and STI and LTI opportunities of 50% of fixed respectively, the change represents an increase in maximum remuneration opportunity of between 2% and 5% (for yield of between 3% and 8% and assuming a 3 year performance period).

Understand the benchmarking

Some boards may not want to remove the disparity and include a dividend entitlement. However, boards should ensure their executives have been benchmarked on a like-for-like basis. In that way, they are best informed for discussions with investors, proxy advisers and their executives.

This means knowing the constituents of the comparator group, their yield profile, their equity policy and how these have been adjusted in the benchmarking to ensure a valid comparison.

© Guerdon Associates 2026

Back to all articles

Back to all articles